Money is not free to borrow. People can always find a use for money, so it costs to borrow money. Different places charge different amounts at different times! It is called Interest. This lesson explains the concept of Simple Interest and Compound Interest. We will develop a basic understanding of these two different types of interests, their uses and properties.

Simple Interest (SI)

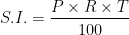

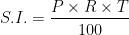

It is an easy and quick method of calculating an interest charge on a loan. Simple interest (S.I.) is determined by multiplying the principal (P) with rate of interest (R) and time period (T).

Example: Henry borrowed Rs. 5000 for 4 years at an interest rate of 5% from a bank. How much of interest is that?

We know,

Here P= Rs. 5000, R= 5%, T= 4 years

So,

Ans: Henry has to pay Rs. 1000 as interest.

Clearly, in S.I. the principal remains constant throughout. But the above method is not generally used in day to day financial system like banks, insurance companies, post offices. They use a different method of computing interest. In this method the lender and the borrower agree to fix up a certain time interval, say a year or half a year or a quarter of a year for the computation of the interest and the amount. At the end of the first interval, the interest is computed and is added to the original principal. The amount obtained is added to the second interval of time. The amount of this principal at the end of the second interval of time is taken as the principal of the third interval of time and so on. At the end of the certain specified period, the difference between the amount and money borrowed, that is, the original principal is computed and it is called the compound interest. Let us simplify it.

Compound Interest (CI)

If the borrower and lender agree to fix up a certain interval of time, so that the amount (Principal + Interest) at the end of the interval becomes the principal of the next interval, then the total interest over all the interests, calculated in this way is called the Compound Interest or C.I..

Evidently, C.I. at the end of a certain specified period is equal to the difference between the amount at the end of the period and the original principal.

C.I. = Amount – Principal

Conversion Period: The fixed interval of time at the end of which the interest is calculated and added to the principal at the beginning of the interval is called the conversion period. In other words, the period at the end of which the interest is compounded is called the conversion period. For instance, when the interest is calculated and added to the principal every six months, the conversion period is six months. Likewise, the conversion period is three months when the interest is calculated and added quarterly.

NOTE: If no conversion period is specified, the conversion period is taken to be one year.

Compound Interest Calculation from simple Interest where Interest is compounded annually.

Q1. Find the Compound interest on Rs. 10000 for two years at 5% per annum.

Solution: Principal for the first year = Rs. 10000

Interest for the first year =

[We are using the formula

Interest for the second year =

Principal of the second year was Rs. 10500 and so amount at the end of the second year = Rs. 10500 + Rs. 525 = Rs. 11025

So, Compound interest= Rs. (11025 – 10000) = Rs. 1025

Note: The C.I. can also be found by adding the interest for each year.

Compound Interest Calculation from simple Interest where Interest is compounded half yearly.

If the rate of interest is R% per annum and the interest is compounded half-yearly, then the rate of interest will be R/2% per half year.

Q: Find the compound interest on Rs. 10000 for 1½ years at 20% per annum, interest being payable half-yearly.

Solution: We know, R= 20% per annum

or, 10% per half year.

T= 1½ years = 3 half years

Original Principal (P) = Rs. 10000

I for the first half-year =

P for the second half-year = Rs. 10000+1000= Rs. 11000

I for the second half-year =

Amount at the end of the second half-year = Rs. 11000 + Rs. 1100 = Rs. 12100

P for the third half year= Rs. 12100

I for the third half-year =

Amount at the end of third half-year = Rs. 12100 + Rs. 1210 = Rs. 13310

Computation of C.I. when Interest is compounded quarterly

If the rate of interest is R% per annum and the interest is compounded quarterly, then the rate of interest will be R/4% per quarter.

Q: Find the compound interest on Rs. 10000 for 1 year at 20% per annum, compounded quarterly.

Solution: We have, R= 20% per annum = 20/4 % = 5% per quarter

T= 1 year= 4 quarters

P for the first quarter= Rs. 10000

Interest for the first quarter =

Amount at the end of first quarter= Rs. 10000 + Rs. 500 = Rs. 10500

P for the second quarter = Rs. 10500

Interest for the second quarter =

Amount at the end of second quarter= Rs. 10500 + Rs. 525 = Rs. 11025

P for the third quarter = Rs. 11025

Interest for the third quarter =

Amount at the end of third quarter = Rs. 11025 + Rs. 551.25 = Rs. 11576.25

P for the fourth quarter = Rs. 11576.25

Interest for the fourth quarter =

Amount at the end of fourth quarter = Rs. 11576.25 + Rs. 578.8125= Rs. 12155.0625

Compound Interest formula

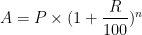

Let P be the principal and the rate of interest be R% per annum. If the interest is compounded annually, the amount A and the compound interest, C.I., at the end of n years is given by

and,

![C.I.= A-P = P \times [( 1 + \dfrac{R}{100})^n - 1]](https://s0.wp.com/latex.php?latex=C.I.%3D+A-P+%3D+P+%5Ctimes+%5B%28+1+%2B+%5Cdfrac%7BR%7D%7B100%7D%29%5En+-+1%5D+&bg=ffffff&fg=000&s=0&c=20201002)

Proof: We have,

P = Principal and rate of interest is R% per annum. Since the interest is given annually.

![P + \dfrac{P \times R}{100} = P [1 + \dfrac {R}{100}]](https://s0.wp.com/latex.php?latex=P+%2B+%5Cdfrac%7BP+%5Ctimes+R%7D%7B100%7D+%3D+P+%5B1+%2B+%5Cdfrac+%7BR%7D%7B100%7D%5D+&bg=ffffff&fg=000&s=0&c=20201002)

Now, this amount is taken as the principal for the second year.

![= P [1 + \dfrac{R}{100}] \times \dfrac{R}{100}](https://s0.wp.com/latex.php?latex=%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D+%5Ctimes+%5Cdfrac%7BR%7D%7B100%7D+&bg=ffffff&fg=000&s=0&c=20201002)

![= P [1 + \dfrac{R}{100}] + P [1+ \dfrac{R}{100}] \times \dfrac{R}{100}](https://s0.wp.com/latex.php?latex=%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D+%2B+P+%5B1%2B+%5Cdfrac%7BR%7D%7B100%7D%5D+%5Ctimes+%5Cdfrac%7BR%7D%7B100%7D+&bg=ffffff&fg=000&s=0&c=20201002)

![= P [1 + \dfrac{R}{100}] \times [1+ \dfrac{R}{100}]](https://s0.wp.com/latex.php?latex=%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D+%5Ctimes+%5B1%2B+%5Cdfrac%7BR%7D%7B100%7D%5D+&bg=ffffff&fg=000&s=0&c=20201002)

![= P [1 + \dfrac{R}{100}]^2](https://s0.wp.com/latex.php?latex=%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5E2+&bg=ffffff&fg=000&s=0&c=20201002)

Considering this amount as the principal of the third year, we have

The interest for the third year

![= P [1 + \dfrac{R}{100}]^2 \times \dfrac{R}{100}](https://s0.wp.com/latex.php?latex=%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5E2+%5Ctimes+%5Cdfrac%7BR%7D%7B100%7D+&bg=ffffff&fg=000&s=0&c=20201002)

![= P [1 + \dfrac{R}{100}]^2 + P [1 + \dfrac{R}{100}]^2 \times \dfrac{R}{100}](https://s0.wp.com/latex.php?latex=%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5E2+%2B+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5E2+%5Ctimes+%5Cdfrac%7BR%7D%7B100%7D+&bg=ffffff&fg=000&s=0&c=20201002)

![= P [1 + \dfrac{R}{100}]^2 \times [1 + \dfrac{R}{100}]^2](https://s0.wp.com/latex.php?latex=%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5E2+%5Ctimes+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5E2+&bg=ffffff&fg=000&s=0&c=20201002)

![= P [1 + \dfrac{R}{100}]^3](https://s0.wp.com/latex.php?latex=%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5E3+&bg=ffffff&fg=000&s=0&c=20201002)

Hence, if we go on like this further, we have

Amount at the end of n years

![= P [ 1 + \dfrac{R}{100}]^n](https://s0.wp.com/latex.php?latex=%3D+P+%5B+1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5En+&bg=ffffff&fg=000&s=0&c=20201002)

Type 1: When the interest is compounded annually

Q: Find the amount of Rs.8000 for 3 years, compounded annually at 10% per annum. Also find the C.I.

Here, P= Rs.8000, R= 10% per annum and n= 3 years.

Using the formula

![A = P [1 + \dfrac{R}{100}]^n](https://s0.wp.com/latex.php?latex=A+%3D+P+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5En+&bg=ffffff&fg=000&s=0&c=20201002)

Amount for 3 years

![= Rs. [8000 \times (1 + \dfrac{10}{100})^3]](https://s0.wp.com/latex.php?latex=%3D+Rs.+%5B8000+%5Ctimes+%281+%2B+%5Cdfrac%7B10%7D%7B100%7D%29%5E3%5D+&bg=ffffff&fg=000&s=0&c=20201002)

![= Rs. [8000 \times \dfrac{11}{10} \times \dfrac{11}{10} \times \dfrac{11}{10}]](https://s0.wp.com/latex.php?latex=%3D+Rs.+%5B8000+%5Ctimes+%5Cdfrac%7B11%7D%7B10%7D+%5Ctimes+%5Cdfrac%7B11%7D%7B10%7D+%5Ctimes+%5Cdfrac%7B11%7D%7B10%7D%5D+&bg=ffffff&fg=000&s=0&c=20201002)

Thus the amount after 3 years is Rs.10,648

And the C.I. = Rs. ( 10648 – 8000 ) = Rs. 2648.

Type 2: When the interest is compounded annually but rates are different for different years.

Let Principal = Rs. P, Time= 2 years, and let the rates of interest be p% per annum, during the first year and q% per annum during the second year.

Then the amount after 2 years

![= Rs.[P \times (1 + \dfrac{p}{100}) \times (1 + \dfrac{q}{100})]](https://s0.wp.com/latex.php?latex=%3D+Rs.%5BP+%5Ctimes+%281+%2B+%5Cdfrac%7Bp%7D%7B100%7D%29+%5Ctimes+%281+%2B+%5Cdfrac%7Bq%7D%7B100%7D%29%5D+&bg=ffffff&fg=000&s=0&c=20201002)

This formula can be similarly extended for any number of years.

Q: Find the amount of R.s. 50000 after 2 years, compounded annually; the rate of interest being 8% p.a. during the first year and 9% p.a. during the second year. Also, find the compound interest.

Here, P = R.s. 50000, p= 8% p.a. and q= 9% p.a.

Using the formula

![A= [P \times (1 + \dfrac{p}{100}) \times (1 + \dfrac{q}{100})]](https://s0.wp.com/latex.php?latex=A%3D+%5BP+%5Ctimes+%281+%2B+%5Cdfrac%7Bp%7D%7B100%7D%29+%5Ctimes+%281+%2B+%5Cdfrac%7Bq%7D%7B100%7D%29%5D+&bg=ffffff&fg=000&s=0&c=20201002)

amount after 2 years

![= Rs. [50000 \times (1 +\dfrac{8}{100}) \times (1 +\dfrac{9}{100})]](https://s0.wp.com/latex.php?latex=%3D+Rs.+%5B50000+%5Ctimes+%281+%2B%5Cdfrac%7B8%7D%7B100%7D%29+%5Ctimes+%281+%2B%5Cdfrac%7B9%7D%7B100%7D%29%5D+&bg=ffffff&fg=000&s=0&c=20201002)

![= Rs. [50000 \times \dfrac{27}{25} \times \dfrac{109}{100}] = Rs. 58860.](https://s0.wp.com/latex.php?latex=%3D+Rs.+%5B50000+%5Ctimes+%5Cdfrac%7B27%7D%7B25%7D+%5Ctimes+%5Cdfrac%7B109%7D%7B100%7D%5D+%3D+Rs.+58860.&bg=ffffff&fg=000&s=0&c=20201002)

And, the C.I. is Rs. [ 58860 – 50000 ] = Rs. 8860.

Type 3: When interest is compounded annually but time is a fraction

Suppose time is

Then, amount

![= P \times [1 + \dfrac{R}{100}]^2n \times [1 + \dfrac{3}{5} \times R ]](https://s0.wp.com/latex.php?latex=%3D+P+%5Ctimes+%5B1+%2B+%5Cdfrac%7BR%7D%7B100%7D%5D%5E2n+%5Ctimes+%5B1+%2B+%5Cdfrac%7B3%7D%7B5%7D+%5Ctimes+R+%5D+&bg=ffffff&fg=000&s=0&c=20201002)

Type 4: Interest Compounded Half-Yearly

Let the Principal be Rs. P, The rate of interest be R% and time be n years.

Suppose the interest is compounded half-yearly. Then,

rate = (R/2) % per half year, time= 2n half-years and amount

![= Rs. [1 + \dfrac{R}{2 \times 100}]^{2n}](https://s0.wp.com/latex.php?latex=%3D+Rs.+%5B1+%2B+%5Cdfrac%7BR%7D%7B2+%5Ctimes+100%7D%5D%5E%7B2n%7D+&bg=ffffff&fg=000&s=0&c=20201002)

Type 5: Interest Compounded Quarterly

Let the Principal be Rs. P, The rate of interest be R% and time be n years.

Suppose the interest is compounded quarterly. Then,

rate= (R/4) % per half year, time= 4n quarters and amount

![= Rs. [1 + \dfrac{R}{4 \times 100}]^{4n}](https://s0.wp.com/latex.php?latex=%3D+Rs.+%5B1+%2B+%5Cdfrac%7BR%7D%7B4+%5Ctimes+100%7D%5D%5E%7B4n%7D+&bg=ffffff&fg=000&s=0&c=20201002)