Many states of India have introduced a new method of realising tax on the sale and purchase of goods. In the earlier form of sales tax, the tax was realized by the government at a single point. The manufacturer or importer of goods (wholesaler or stockist) was liable to pay sales tax to the government. In the new VAT system, the tax is realized by the government at many points in the supply chain, right from the manufacturer to the retailer. Only the value added to the commodity at each stage is subjected to sales tax. The final incidence of sales tax remains with the consumer.

Let us consider an example. A retailer purchases an article for Rs 100 from the wholesaler. The wholesaler charges a sales tax at the rate of 10% on it as prescribed by the government for that variety of articles. Thus, the retailer pays Rs 100 + 10% of Rs 100, i.e., Rs 100+Rs 10 (=Rs 110) to the wholesaler to have the article. The wholesaler gets Rs 100 and he pays Rs 10 to the government as sales tax. The retailer sells the article for Rs 120 to the consumer and charges a sales tax of 10% on it as prescribed by the government. Thus, the consumer pays Rs 120 + 10% of Rs 120, i.e., Rs 120+Rs 12 (=Rs 132) to the retailer to get the article. The retailer gets Rs 120+Rs 10, i.e., Rs 130 after paying Rs 12-Rs 10, i.e., Rs 2 as sales tax to the government. In this way the retailer pays 10% of (sale price-cost price), i.e., (Rs 120-Rs 100) to the government. Thus the retailer pays the tax on the added (raised) value of the article only. So, the value-added tax (VAT) for the retailer in this case is Rs 2. The above example may be summarized as below:

For the retailer, we have:

Purchase price = Rs 100

Tax paid on purchase = Rs 10 (This tax is called input tax.)

Sale price = Rs 120

Tax payable on sale price = Rs 12 (This tax is called output tax.)

Input tax credit = Rs 10

So, VAT payable by the retailer = output tax-input tax=Rs 12-Rs10=Rs 2

Points to Remember:

- VAT is the short form of Value Added Tax.

- VAT=output tax-input tax.

- VAT is not in addition to the existing sales tax, but is the replacement of sales tax. Presently majority state governments have accepted VAT system but some are still continuing with sales tax.

- VAT is a tax on the value added at each transfer of goods, from original manufacturer to the ultimate customer.

- VAT is calculated on the sale value by applying the rate of tax as applicable.

Examples

Example 1: A retailer buys an article from the wholesaler at Rs 80 and the wholesaler charges a sales tax at the rate prescribed rate of 8%. The retailer fixes the price at Rs 100 and charges sales tax at the same rate. Apply VAT system of sales tax calculation to answer the following.

(i) What is the price that a consumer has to pay to buy the article?

(ii) Find the input tax and output tax for the retailer.

(iii) How much VAT does the retailer pay to the government?

Solution:

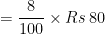

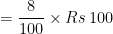

(i) Here, the price P=Rs 100 and the rate of sales tax r%=8%

(ii) Input tax= Tax paid by the retailer to the wholesaler

Output tax= Tax realised by the retailer from the consumer

(iii) VAT paid by the retailer = Output tax – Input tax

=Rs (8-6.40)

=Rs 1.60

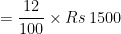

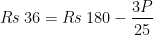

Example 2: A shopkeeper sells an article whose listed price is Rs 1500 and charges sales tax on it at the prescribed rate of 12% from the consumer. If the shopkeeper pays a VAT of Rs 36 to the government, what was the price inclusive of tax at which the shopkeeper bought the article from the wholesaler?

Solution:

Here, Output tax= Tax realised by the retailer from the consumer

Let the price of the article charged by the wholesaler be P before tax.

Then the input tax

Now,

VAT= Output tax-Input tax

Example 3: A manufacturer printed the price of his goods as Rs 120 per article. He allowed a discount of 30% to the wholesaler who in his turn allowed a discount of 20% on the printed price to the retailer. If the prescribed rate of sales tax on the goods is 10% and the retailer sells it to the consumer at the printed price then find the VATs paid by the wholesaler and the retailer.

Solution:

For the manufacturer, the price of the article at which it is sold

=printed price-discount to the wholesaler

For the wholesaler, the price of the article at which it is sold

=printed price-discount to the retailer

So, VAT payable for the wholesaler

=output tax-input tax

=Rs (9.60-8.40)

=Rs 1.20

For the retailer, the price of the article at which it is sold

=printed price

=Rs 120

Therefore, output tax for the retailer=10% of Rs 120= Rs 12

Input tax for the retailer= output tax for the wholesaler= Rs 9.60

So, VAT payable by the retailer=output tax-input tax

=Rs (12-9.60)

= Rs 2.40

Therefore, VAT paid by the wholesaler is Rs 1.20 and that paid by the retailer is Rs 2.40.

Exercise

- A shopkeeper buys an article from the wholesaler at Rs 72 and pays sales tax at the rate of 10%. The shopkeeper fixes the price of the article at Rs 90 and charges sales tax at 10% from the consumer. Apply VAT system of sales tax calculation to answer the following:

- Find the input tax and output tax for the shopkeeper.

- Find the VAT that the shopkeeper pays to the government.

- Find the profit per cent made by the shopkeeper.

- A shopkeeper purchases an article for Rs 6200 and sells it to a customer for Rs 8500. If the VAT rate is 8%, find the VAT paid by the shopkeeper.

- A shopkeeper buys 10 phials of a medicine for Rs 560 and pays sales tax at the prescribed rate of 4%. He sells 6 phials at Rs 65 per phial and charges sales tax from the buyer at the prescribed rate. Find the input tax and output tax for the shopkeeper against the sale of 6 phials. Also, find the VAT payable by the shopkeeper.

- A purchases an article for Rs 3600 and sells it to B for Rs 4800. B, in turn, sells the article to C for Rs 5500. If the VAT rate is 10%, find the VAT levied on A and B.

- A man buys an article whose listed price is Rs 380 from a shopkeeper and pays a sales tax at the rate of 10%. The shopkeeper pays a VAT of Rs 3. Find the input tax and the price inclusive of tax at which the shopkeeper bought the article from the wholesaler.

- A manufacturer lists the price of his goods at Rs 2400 per article. The wholesaler gets a discount of 25% on the goods from the manufacturer. The retailers are allowed a discount of 15% on the listed price by the wholesaler. The prescribed rate of sales tax at all stage is 8%. A consumer buys an article from the retailer at the listed price. Find the VATs paid by the wholesaler and the retailer.

- A retailer charges sales tax on an article at the rate of 6% from the buyer. The listed price of the article is Rs 450. If the retailer has to pay a VAT of Rs 2.40, what was the sum the retailer paid to the wholesaler?

- A manufacturer buys raw material for Rs 60000 and pays 4% tax. He sells the ready stock for Rs 92000 and charges 12.5% tax. Find the VAT paid by the manufacturer.

- Rohit has a furniture shop in Delhi. He buys a dining table for Rs 12000 and sells it to a customer for Rs 15000. Find the VAT paid by Rohit, if the VAT rate is 10%.

- A manufacturer fixed the price of an article at Rs 250. The rate of sales tax on the article is 12%. A wholesaler bought it and sold the same to a shopkeeper at a profit of 10%. The shopkeeper sold the article to a consumer at a profit of 15 per cent. Find the sum of money the consumer paid to buy the article and the VAT paid by the wholesaler and the retailer together.